Quidkey: A Global Clearing House for Modern Payments

COO Bhavna Saraf explains how Quidkey uses APIs and AI to transform open banking into merchant-ready A2A payment solutions.

4 min read·Read article→

AI agents can do real work but can’t safely spend money. Bounded financial authority is the last missing primitive — and it’s hiding in plain sight.

There’s a shift happening in how software operates. Until recently, AI systems were assistants: they could suggest, summarize, draft, and help humans move faster. They were co-pilots. The human was still in the seat.

That’s changing.

Agents today can persist across sessions, use tools, coordinate with other systems, and complete real parts of workflows without constant human involvement. They’re booking meetings, deploying code, managing inboxes, running research pipelines. The line between "AI helps me do the work" and "AI does the work" is collapsing faster than most people expected.

But there’s a problem almost no one is talking about. Once an agent can actually complete work end to end, it almost immediately needs to spend money.

A developer agent needs to pay for compute or API access. A research agent needs to buy a dataset. An operations agent needs to settle a vendor invoice. A personal assistant agent needs to book travel. The moment autonomous software touches a real workflow, payment becomes part of that workflow.

And right now, every company trying to deploy agents faces an impossible choice.

Option one: give the agent access to a company card or shared banking credentials. It’s the fastest shortcut and the worst long-term answer. There’s no per-agent isolation, no clean way to limit damage if the agent is compromised, and no good way to attribute spend or revoke access. If something goes wrong, the blast radius is too large.

Option two: keep a human in the loop for every payment. Safer, yes. But this turns agents back into suggestion engines. The entire point of autonomous systems is that they should be able to complete bounded work on their own. If every payment still requires human approval, the autonomy breaks exactly where it matters most.

Most teams stuck between these options are essentially left with agents that can do almost everything — except finish the loop.

This isn’t a narrow edge case. Juniper Research recently projected that agentic commerce spend could reach $1.5 trillion globally by 2030. The autonomy is arriving. The financial infrastructure isn’t.

The tempting answer is that something already covers this. It doesn’t.

The common thread: every existing approach was built for humans first and stretched toward software. They all assume a person is making judgment calls somewhere in the loop. Autonomous software needs a different primitive entirely.

That means a few things working together. Each agent should have its own isolated wallet — its own balance, ledger, credentials, and policy boundary. If one agent is compromised or behaves unexpectedly, the damage stops there. It can’t affect other agents or the company’s operating accounts.

The rules governing that wallet need to be enforced by infrastructure, not by prompts. Budgets, transaction limits, velocity controls, merchant restrictions, approval thresholds — evaluated outside the agent, in real time, before money moves. A well-designed policy engine means that even if an agent is manipulated into attempting a bad transaction, the financial controls still hold.

When a card is required — because many merchants still need one — agents shouldn’t get reusable corporate cards sitting in their environment. They should be able to request an on-demand, single-use virtual card scoped to a specific transaction, a specific amount, a short time window. One use, then gone.

And the whole system needs to work at scale. Not for one carefully supervised demo agent, but for dozens or hundreds operating under different policies, different budgets, different business contexts.

There’s one more piece most people haven’t thought about yet: the receiving side.

When an agent initiates a transaction, the counterparty has no idea what it’s dealing with. Is this agent real? Is it acting on behalf of a legitimate business? Is it funded? Is it authorised to make this payment?

As agent-based commerce grows, that lack of trust becomes a serious blocker. The answer isn’t just better payment rails — it’s a verification layer that lets counterparties confirm an agent is active, backed by a verified principal, funded, and acting within the scope of its authorisation.

Over time, this becomes the trust and settlement layer for agent commerce — analogous to what card networks do for human commerce today, but built for programmatic actors from the ground up.

The agent economy won’t run on prompts alone.

Every other layer of infrastructure for autonomous software is advancing rapidly. But financial authority — the ability for software to safely spend and receive money in the real economy — is still missing. It’s the last major primitive that hasn’t been built yet.

The companies that figure this out early will unlock workflows that are genuinely blocked today. Not because the agents aren’t capable, but because the financial plumbing was never designed for them.

COO Bhavna Saraf explains how Quidkey uses APIs and AI to transform open banking into merchant-ready A2A payment solutions.

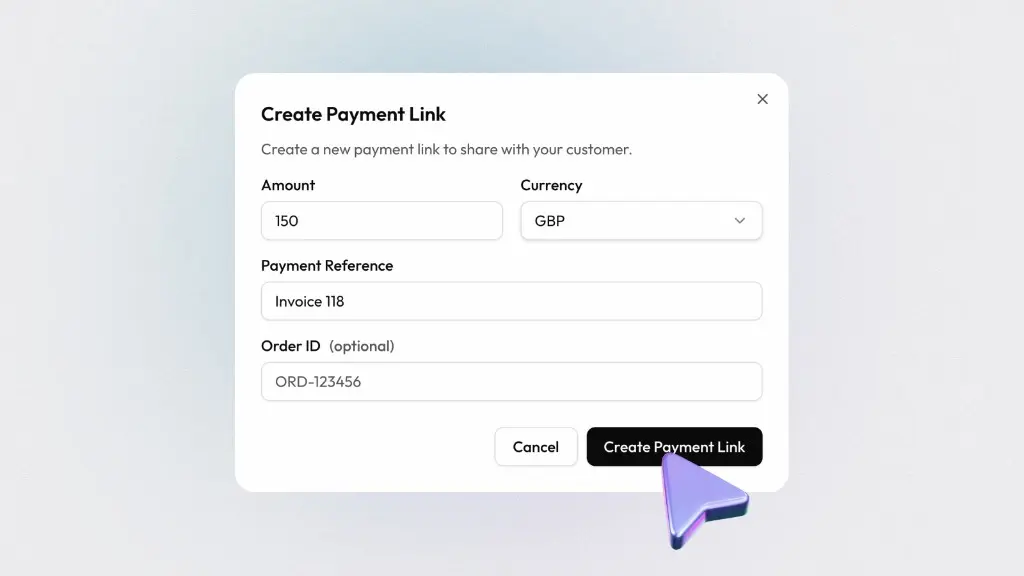

Quidkey Payment Links let businesses request instant Pay by Bank payments with a shareable link, real-time tracking, and no integration required.